New Chapter 11 - Remington Outdoor Company

Remington Outdoor Company

3/25/18

Remington Outdoor Company, a gun manufacturer, has finally filed for bankruptcy - a day after Americans took to the streets to #MarchforourLives. Ah, bankruptcy irony. The company's operations are truly national in scope; it has manufacturing facilities in New York and Alabama and a primary ammunition plant in Arkansas. Its "principal customers are various mass market retail chains (e.g., Wal-Mart and Dick's Sporting Goods) and specialty retail stores (e.g., Bass Pro Shops and Cabela's) and wholesale distributors (e.g., Sports South)." Guns! #MAGA!!

Why did the company have to file for bankruptcy? We refer you to our mock "First Day Declaration" from February here. Much of it continues to apply. Indeed, our mockery of the change in tone from President Obama to President Trump was spot on: post Trump's election, the company's inventory supply far exceeded demand. The (fictional) threat of the government going house-to-house to collect guns is a major stimulant to demand, apparently. Here is the change in financial performance,

"At the conclusion of 2017, the Debtors had realized approximately $603.4 million in sales and an adjusted EBITDA of $33.6 million. In comparison, in 2015 and 2016, the Debtors had achieved approximately $808.9 million and $865.1 million in sales and $64 million and $119.8 million in adjusted EBITDA, respectively."

Thanks Trump.

We'd be remiss, however, if we didn't also note that NOWHERE in the company's bankruptcy filings does it mention the backlash against guns or the company's involvement in shootings...namely, the one that occurred in Las Vegas.

The company, therefore, negotiated with its various lenders and arrived at a restructuring support agreement. The agreement provides for debtor-in-possession credit ($193mm asset-backed DIP + $100mm term loan DIP + $45mm DIP, the latter of which is a roll-up of a bridge loan provided by lenders prior to the filing). Upon the effective date of a plan of reorganization, the third lien lenders and term lenders will own the reorganized company.

- Jurisdiction: D. of Delaware

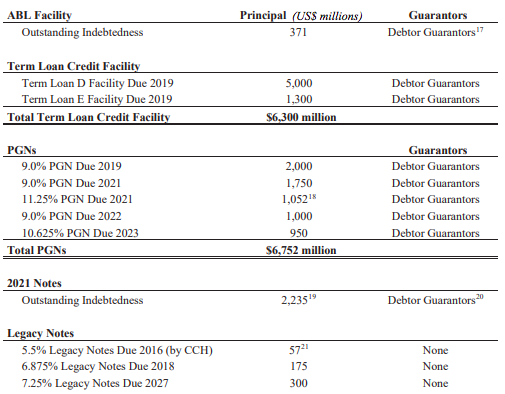

- Capital Structure: $225mm ABL (Bank of America, $114.5mm funded), $550.5mm term loan (Ankura Trust Company LLC), $226mm 7.875% Senior Secured Notes due 2020 (Wilmington Trust NA), $12.5mm secured Huntsville Note

- Company Professionals:

- Legal: Milbank Tweed Hadley & McCloy LLP (Gregory Bray, Tyson Lomazow, Thomas Kreller, Haig Maghakian) & (local) Pachulski Stang Ziehl & Jones LLP (Laura Davis Jones, Timothy Cairns, Joseph Mulvihill)

- Financial Advisor: Alvarez & Marsal LLC (Joseph Sciametta)

- Investment Banker: Lazard (Ari Lefkovits)

- Claims Agent: Prime Clerk LLC (*click on company name above for free docket access)

- Other Parties in Interest:

- DIP ABL Agent ($193mm): Bank of America NA (DIP ABL Lenders: Bank of America NA, Wells Fargo Bank NA, Regions Bank, Branch Banking and Trust Company, Synovus Bank, Fifth Third Bank, Deutsche Bank AG New York Branch)

- Legal: Skadden Arps Slate Meagher & Flom LLP (Paul Leake, Shana Elberg, Jason Liberi, Cameron Fee)

- Admin Agent to the DIP TL: Ankura Trust Company LLC

- Legal: Davis Polk & Wardwell LLP (Damian Schaible, Darren Klein, Michele McGreal, Dylan Consla) & (local) Richards Layton & Finger LLP (Mark Collins, Michael Merchant, Joseph Barsalona)

- Ad Hoc Group of TL Lenders

- Legal: O'Melveny & Myers LLP (John Rapisardi, Andrew Parlen, Joseph Zujkowski, Amalia Sax-Bolder) & (local) Richards Layton & Finger LLP (Mark Collins, Michael Merchant, Joseph Barsalona)

- Third Lien Noteholders

- Legal: Willkie Farr & Gallagher LLP (Rachel Strickland, Joseph Minias, Debra McElligott) & (local) Young Conaway Stargatt & Taylor LLP (Edmon Morton, Allison Mielke)

- Wells Fargo Bank NA

- Legal: Otterbourg PC (Andrew Kramer)

- Cerberus Operations and Advisory Company, LLC

- Legal: Schulte Roth & Zabel LLP (David Hillman)

- Reorganized Board of Directors (Anthony Acitelli, Chris Brady, George W. Wurtz III, G.M. McCarroll, Gene Davis, Ron Coburn, Ken D'Arcy)

- DIP ABL Agent ($193mm): Bank of America NA (DIP ABL Lenders: Bank of America NA, Wells Fargo Bank NA, Regions Bank, Branch Banking and Trust Company, Synovus Bank, Fifth Third Bank, Deutsche Bank AG New York Branch)

- Official Committee of Unsecured Creditors

- Legal: Fox Rothschild LLP (Michael Menkowitz, Paul Labov, Jason Manfrey, Jesse Harris, Seth Niederman)

Updated: 4/27/18