🔋New Chapter 11 Bankruptcy Filing - Exide Holdings Inc.🔋

Exide Holdings Inc.

May 19, 2020

Georgia-based Exide Holdings Inc. and four affiliates (the “debtors”), among the world’s largest producers and recyclers of lead-acid batteries used in cars, boats, golf carts and more, filed for chapter 11 bankruptcy in the District of Delaware earlier this week. The filing sparked an entire industry to ask “is it a Chapter 22 or a Chapter 33?” The answer, depending upon your look-back period, is the latter. The fairer answer is probably the former and even that was 7 years ago with emergence 5 years ago (PETITION Note: the Exide Creditors’ Liquidating Trust had to make a notice of appearance in these new cases so, there’s that). Going back nearly two decades seems to be an impossible standard to hold any business to but 5-7 years seems much fairer.

Since we’re discussing labels, here’s another one: failure. Per the debtors:

Notwithstanding the Company’s efforts to implement its business plan following its emergence from the 2013 Chapter 11 Case and the support of its new owners and lenders, the Company continued to face liquidity, performance, and operational challenges that were more persistent and widespread than anticipated. Coupled with adverse industry and market factors as well as substantial environmental costs, these challenges have resulted in reduced liquidity.

Sooooo…that sucks. We admit it: we were hoping that this was a disruption story. That Elon Musk and the increasingly large cohort of lithium-ion battery using OEMs pushing out electric vehicles were putting the lead-acid battery manufacturers out to pasture. But that is not a state reason for this chapter 3…uh…chapter 2…uh, whatever the f*ck this is. Rather, the debtors state that their post-emergence liquidity issues stem from (a) mounting environmental remediation costs and litigation, (b) rising production costs (PETITION Note: because the debtors shut two recycling facilities, they are now subject to pricing pressures from outside manufacturers rather than just using their own recycled inputs), (c) operational inefficiencies caused by legacy mixed-use facilities, and (d), of course…wait for it…COVID-19. Duck for COVID-cover folks! The debtors say that the pandemic’s impact on demand for product is the cherry on top.

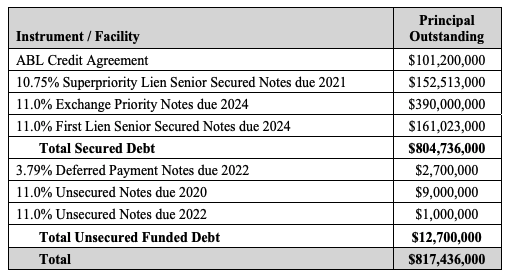

The debtors’ capital structure doesn’t help. Look at this beaut:

With that much funded debt, the debtors’ leverage ratio stands at 9.2x. Debt service averages approximately $26.8mm/year.

So, confronted with all of these factors, the debtors have been engaged in a marketing process since 2018. The continued deterioration of the business, however, ultimately led to a restructuring path and now the debtors intend to use the bankruptcy process to effectuate a sale of (i) the entire business or (ii) the Americas business and/or (iii) the sale of its Europe/Rest-of-World business or (iv) a liquidation (PETITION Note: the debtors fall into chapter 11 largely separated into four main business groups). The Ad Hoc Group has submitted a binding credit bid for the Europe/ROW business group which will serve as a stalking horse bid; they have also committed $15mm in DIP financing to service certain non-debtor affiliates in Europe with an additional $25mm DIP commitment for the administration of the cases coming from Blue Torch Capital LP. The debtors hope to go “effective” by the end of August: this means that everyone has a lot of work to do to try and and locate a buyer for the rest of the debtors’ businesses in the interim.

Jurisdiction: D. of Delaware (Judge Sontchi)

Capital Structure:

Professionals:

Legal: Weil Gotshal & Manges LLP (Ray Schrock, Jacqueline Marcus, Sunny Singh, Samuel Mendez, Alyssa Kutner, Jason Hufendick) & Richards Layton & Finger PA (Daniel DeFranceschi, Zachary Shapiro, Brendan Schlauch)

Independent Directors: Alan Carr, William Transier, Harvey Tepner, Mark Barberio

Financial Advisor/CRO: Ankura Consulting (Roy Messing)

Investment Banker: Houlihan Lokey Capital Inc.

Claims Agent: Prime Clerk LLC (*click on the link above for free docket access)

Other Parties in Interest:

Prepetition ABL Agent: Bank of America NA

Legal: Otterbourg PC (Daniel Fiorillo, David Morse, Jonathan Helfat)

Indenture Trustee

Legal: Arent Fox LLP (Andrew Silfen, Jordana Renert)

DIP Agent ($40mm): Blue Torch Capital LP

Legal: Gibson Dunn & Crutcher LLP (Robert Klyman, Matthew Bouslog, Michael Farag) & Cole Schotz PC (Norman Pernick, Patrick Reilley)

Ad Hoc Group

Legal: Paul Weiss Rifkind Wharton & Garrison LLP (Alice Belisle Eaton, Robert Britton, Eugene Park, Claudia Tobler, Jacqueline Rubin, Douglas Keeton, David Weiss, David Giller) & Young Conaway Stargatt & Taylor LLP (Pauline Morgan, Sean Greecher, Andrew Magaziner, Ian Bambrick)

Large equityholders: Mackay Shields LLC, AllianceBernstein LLP, D.E. Shaw Galvanic Portfolios LLC, Neuberger Berman Group LLC

Exide Creditors’ Liquidating Trust

Legal: Kelley Drye & Warren LLP (Dane Kane, Konstantinos Katsionis)