December 19, 2018

A week after Glossier CEO Emily Weiss revealed that the direct-to-consumer beauty brand hit $100mm in sales, Glansaol, a platform company that acquires, integrates and cultivates a portfolio of prestige beauty brands — including a direct-to-consumer brand — filed for bankruptcy in the Southern District of New York. The company owns a trio of three main brands: (a) Laura Geller, a distributor of female beauty and personal care products sold primarily on QVC and wholesale, (b) Julep, a wholesale distributor of high-end nail polish, skincare and cosmetic products with a direct-to-consumer and “subscription box” model, and (c) Clark’s Botanicals, a skincare retailer, which sells primarily via e-commerce (including Amazon) and QVC.

The company indicated that “a general shift away from brick-and-mortar shopping, evolving consumer demographics, and changing trends” precipitated its bankruptcy filing. More specifically, profit drivers, historically, have been broadcast shopping networks and wholesale distribution. But both QVC and large retailers have cut back orders significantly amidst a broader industry shakeout. Compounding matters is the fact that the company’s top two customers account for over 60% of total receivables. As we always say, customer concentration is NEVER a good thing.

Moreover, the company added:

…the Debtors have been unable to replace key revenue generators due to: (a) the increasingly competitive industry landscape coinciding with the downturn in the brick and mortar retail sector; (b) the decline in broadcast shopping network sales; and (c) the downturn of the Company’s single-brand subscription business, which faces competition from new entrants that offer subscriptions covering a variety of brands.

Hmmm. Insert Birchbox here? Perhaps Glansaol ought to have entered into a partnership with Walgreens! 🤔

What happens when you can’t move product? You build up inventory. Which, for a variety of reasons, is no bueno. Per the company:

…the decline in sales has saddled the Debtors with a significant oversupply of inventory, which has forced the Debtors to sell goods at steep markdowns and destroy certain products, further tightening margins and draining liquidity. Oversupply of inventory, coupled with higher returns and chargebacks described below, has also significantly increased the Debtors’ costs for warehouses and other third-party logistics providers.

Interestingly, the company aggregated the three brands in the first place because of perceived supply chain synergies. Per the company:

The strategy was put into practice in late 2016 and early 2017 when the Debtors acquired a trio of rising prestige beauty companies ― Laura Geller, Julep, and Clark’s Botanicals. The combination was designed to realize the benefit of natural synergies without any cannibalization. The brands share relatively similar supply chains where it was thought efficiencies could be realized, but they featured different price points and consumer profiles. For example, while Laura Geller appeals to consumers over the age of 35 and is primarily sold through wholesale retailers and broadcast shopping networks, Julep caters to a younger generation through its online business and experience-driven nail salons.

We love synergies. They always seem to be good in theory and nonexistent in practice. To point:

the Debtors were never able to achieve significant cost savings related to shared services among their brands. Upon the Debtors’ acquisitions of Laura Geller, Julep and Clark’s in 2016, the plan was to ultimately consolidate shared services, including supply chain, senior management, administrative support, human resources, information technology support, accounting, finance and legal services. The brands, however, were never fully integrated. Instead, the Company is saddled with a substantial legacy investment in a new ERP system, which was put into place ahead of cross-organizational efficiency initiatives and right-sizing functionality. Accordingly, the costs savings attributed to synergies, which had been a pillar of the Debtors’ original business model, were never realized.

Which is why we generally tend to be skeptical whenever we hear about cost savings and synergies as a basis for M&A (cough, Refinitiv).

Given all of the above, the company has been engaged in a marketing process since roughly February 2018 running, in the interim, based on its credit facility and equity infusions. Now, though, the company has a stalking horse bidder in tow in the form of AS Beauty LLC, which has agreed to purchase the company’s brands and related capital assets for approximately $16.2mm. The company’s prepetition lender, SunTrust Bank, has agreed to provide a $15mm DIP credit facility which, along with cash collateral, will fund the cases.

Jurisdiction: S.D. of New York (Judge Wiles)

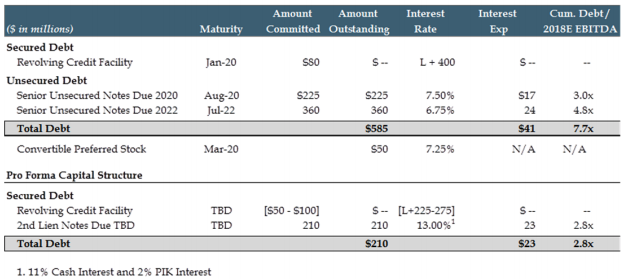

Capital Structure: $7.2mm RCF (SunTrust Bank)

Company Professionals:

Legal: Willkie Farr & Gallagher LLP (Brian Lennon, Daniel Forman, Andrew Mordkoff)

Financial Advisor: Emerald Capital Advisors (John Madden)

Claims Agent: Omni Management Group Inc. (click on the case name above for free docket access)

Other Parties in Interest:

Prepetition Secured & DIP Lender: SunTrust Bank (Legal: Parker Hudson Rainer & Dobbs LLP — Rufus Dorsey, Eric Anderson, James Gadsden

Stalking Horse Purchaser: AS Beauty LLC (Legal: Sills Cummis & Gross PC — Michael Goldsmith, George Hirsch)

Private Equity Sponsor: Warburg Pincus Private Equity XII Funds