Automation. We hate to pick on support staff as there's been a lot of pain there the past decade but...short administrative assistants? On the flip side, note this.

European Distressed Debt. The vultures are looking at Spain and Italy. Meanwhile, last week Agent Provocateur, this week Jones Bootmaker = the latest PE-backed European retailer staring down the brink of administration(with KPMG hired to find a buyer).

Grocery. Food deflation appears to be leveling off - good news for grocers who had a rough 2016 (which we covered previously here).

Guns. Looks like the rise in anti-Semitism and hate crimes hasn't translated into robust gun sales: Remington Arms Co. is downsizing. The $2.6mm trade claim the company has in the Gander Mountain Company bankruptcy won't help matters either.

Restaurants. Ruby Tuesday is now for sale after closing 100 locations. UBS is apparently the financial advisor.

Retail. Shocker! A newly released report delineating the most valuable retail brands failed to include Charming Charlie's, Payless Shoes, rue21, J.Crew...ah, you get the point. Also notably absent from this list is Neiman Marcus which, given its lack of scale (42 stores, ex-Last Call & Bergdorf Goodman), isn't all too surprising on a relative basis but that hasn't stopped it from attracting attention from Hudson's Bay Co (note: the Canadians have been taking a lot of interest in US retail lately, see, also Eastern Outfitters). Looks like some teens DO shop at Neiman Marcus but find malls, generally, "vanilla"...choice quote here: "I like finding stuff on eBay - clothes and accessories that no one else is wearing...[e]verything you can't find in a mall." See, also, Poshmark. Meanwhile, private equity backed retail is especially sordid.

Retail II. Bon Ton Stores (BONT) reported higher earnings, cost savings that bested projections and a free cash flow positive '16 (compared to a wildly cash flow negative '15). But same store sales were down big. A few takeaways: 1) bad retail performance is always partially the weather's fault; 2) it's planning to make its landlords sweat with lease negotiations; 3) it's closing 46 stores in '17; 4) it's picking from the carcass of closed Macy's locations, poaching vendors and sales associates; and 5) it's still over-levered AF. While there is no near-term maturity post-retirement of the '17 second lien senior secured notes and the company claims liquidity through '17, the company is still levered at 8.5x and raising rates, generally, won't help retail. And the stock trades in dogsh*t (reverse split?) territory at $1.00. Hmmmmm.

Fast Forward: iHeartMedia launched an optimistic restructuring process seeking to swap more than 90% of its $20b of debt; Gymboree got a going-concern warning in the face of declining revenue and same-store sales and a 12/17 maturity; Gulfmark Offshore skipped its interest payment triggering a 30-day grace period due 4/15; the same date marks the forbearance expiration agreed to by lenders of 21st Century Oncology; and Concordia International Corp. reported HORRIBLE numbers and declined to provide go-forward guidance given the headwinds confronting drug pricers.

Rewind I: We swear we're not picking onSun Capital Partners but this week S&P Global Ratings downgraded Vince Intermediate Holdings to CCC+ making SCP's portfolio a virtual retail minefield.

Rewind III: Last week we covered Aquion Energy in our summaries of cases (click company name for summary). Turns out, this dog is more controversial than we thought as its another example of government subsidy gone wrong. Which is not to say we're not for experimentation/funding with/for alternative energy businesses, particularly in storage. But the comments to this seem on point.

Malls. Kenneth Rosen of Lowenstein Sandler LLP discusses the need for malls to diversify given a multitude of challenges to retail.

Marblegate/TIA - King & Spalding LLP's Michael Rupe, W. Austin Jowers, Jeffrey Pawlitz, Christopher Boies and Michael Handler offer their thoughts on the recent much-discussed ruling on the Trust Indenture Act.

Subordination. Michael Friedman and Leo Gagion of Chapman & Cutler LLP discuss the recent Ninth Circuit decision on subordination.

Survey. AlixPartners released its 2017 restructuring experts survey. Read it here. And here is a summary.

Coal. Prices have risen and Trump is promising assistance. Is this enough to offset sagging demand? China's new measures aren't helping. But the capital markets are, as Peabody Energy, Arch Coal, and Contura Energy are all taking advantage of cheap financing/refinancing options. Peabody shopped an upsized term loan (by $450mm) with revised company-favorable pricing; it also issued new notes and bonds. Amazing how quickly things changed with coal.

Electric Vehicles. Something tells us that oil and gas management teams and their wildly astute restructuring bankers and advisors neglected to bake this element into their business plans.

European Debt. Increasing concerns about Italy and Greece. Meanwhile, in France, CVC Capital Partners' owned vehicle leasing firm Fraikin has hired Rothschild to restructure its 1.4 billion Euro debt. Lazard will represent the mezz debt.

Moelis & Co. & Aramco. "Ken of Arabia"? C'mon, that's just dumb.

Retail. And people wonder why private equity is vilified...case and point: Rackspace. Speaking of private equity, Canada Goose's proposed IPO reeks of a dump-and-run on greater fools. Millennials don't spend money, but Bain Capital will have us believe that $900 fur-lined jackets are the exception to the rule. Riiiight.

Retail Part IV. Amazon announced that the number of third-party sellers on its B2B site has reached 45k, up about 50% from the approx 30k sellers it had at the end of Q2...IN JUNE.

Return of the Maturity Wall. Nothing gets restructuring professionals' juices flowing like sexy maturity stats. So, here it is: $2 trillion of corporate debt comes due in five years. And this is, in part, because the capital markets are definitely wide open right now in the face of soon-to-be rising interest rates. Take THAT wall, President Trump!

Sears. Everyone is looking at this oncoming trainwreck and wondering "when?", not "if." Nice recent CDS movements on it but then the company unearthed a remarkable $1b in cost savings. Like, out of nowhere. And, naturally, the stock soared 25+%.

Spotify. Typically there are tremors before the earthquake. Perhaps Filip Technologies, Violin Memory, and Nasty Gal are the tremors foreshadowing a venture debt-backed reckoning on the horizon. It's unclear. But, in Spotify's case, the interest ratchets attached to $1b of debt get more and more expensive with each consecutive quarter sans IPO. A big "unicorn" is going to fail and fail big. Spotify may not be the one, but it ain't looking great. But that one IS coming (Zenefits anyone?). Along these lines, how the eff is Theranos not bankrupt yet?

Fast Forward: Most retail-focused restructuring pros emphasize "omni-channel," the latest retail buzzword that, practically speaking, means basically nothing in today's climate. Case and point: Neiman Marcus, which was downgraded this week with projected 10x leverage on $4.77b of debt. Most of the cap stack traded at new lows this week. Omni-channel ain't a panacea, it appears.

Rewind I: This result for Relativity Media sure sounds positive.

Rewind II: The grocery space is getting hammered so badly that now even Whole Foods is retrenching, shutting more stores than it's opening go-forward.

Athleisure. Start the funeral dirge. Under Armourreported dreadful numbers and guided poorly, citing the Sports Authority bankruptcy as a reason for decreased exposure to product. Then S&P kicked UA while it was down, downgrading its corporate credit rating from investment grade to high yield. It's not a restructuring candidate with double-digit growth but its results don't bode well for retailers, generally. Good thing J.Crew is NOW starting to focus on athleisure.

Solar. The technology continues to take hold and grab share but there'll be a lot of carnage along the way. Meanwhile, Exxon got pummeled, noting over $2b in writedowns.

Retail. As distressed investors and bankruptcy professionals lick their chops over the possibilities with rue21, True Religion, Claire's Stores, J.Crew and others, "fast fashion" gets a second look as a culprit in the demise of retail (adding to the typical Amazon narrative). Still, even H&M and Uniqlo have announced intentions to scale back growth plans and/or close stores in the US.

More Retail. The Finish Line Inc. announced its sale of Jack Rabbit Sports this week (66 locations) for undisclosed terms. "Undisclosed terms" = GU gels and a jock-strap. Peter J. Soloman served as financial advisor. The quote, "The acquisition eases fears that the chain would face liquidation with no strategic buyers for the business"...basically sums up specialty retail. Reasons for the company's struggles are particular to specialty running stores, including, notably a marked decline in marathon participation. It's just not that easy to take a selfie while running 26.2.

Morer Retail - Canada. Once high-flying e-commerce startup Shoes.comcapitulates under the weight of multiple lawsuits, thwarting an IPO. In addition to shutting down the e-comm channels, the Vancouver-based company will shut down two brick-and-mortar locations - effectively flushing $45mm of PE down the toilet. Still, that URL seems like it would fetch some value...

Rewind I: Usually we reserve "rewind" for topics we've discussed in previous weeks but we're making an exception here: apparently HMV still exists in Canada. Or did. What a major blast to the past. What were they selling, exactly, 8-tracks?

Rewind II: Payless Shoes. 4400 stores? Wow. Apropos, retail now the sector with the most distressed debt. In other retail news worth a rewind, Sports Direct is reportedly in talks to acquire Eastern Outfitters, the parent company of Bob's Stores and Eastern Mountain Sports from Versa Capital Management out of bankruptcy. If those names sound familiar, it's because Versa literally just bought them in bankruptcy last year in the Vestis Group case. So, add this to the growing list of Chapter 22 cases.

Rewind III: Given our revelation last week of the connection between Puerto Rico-Dentons-New Gingrich, its intriguing that Greenberg Traurig is distancing itself from another Trump supporter.

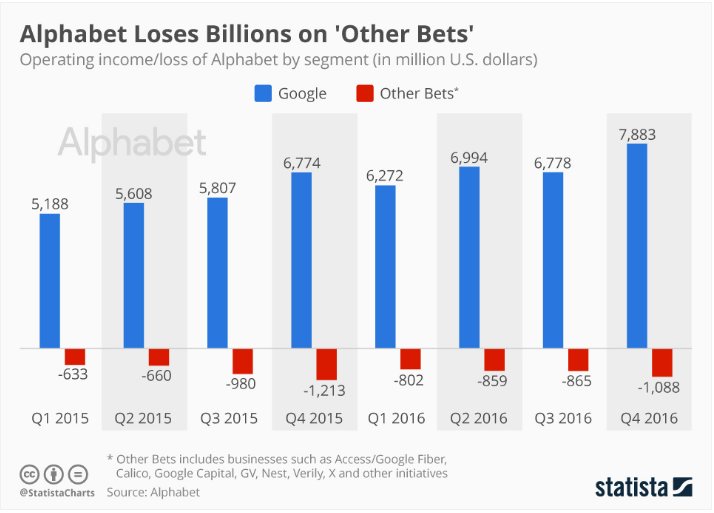

Chart of the Week: Sometimes to disrupt the incumbents, you have to bleed cash like nobody's business...

DIP Carveout. Aaron Stulman of Ashby & Geddes summarizes the recent DE opinion indicating that a DIP carveout does not limit a UCC's professional fees post-confirmation.