Gibson Dunn & Crutcher LLP. Better late than never, we guess. The firm has announced the acquisition/growth of its oil and gas team down in Houston.

Goldman Sachs. Somehow its poor quarterly performance - largely due to poor distressed desk trades - is Morgan Stanley's fault.

Lazy Media. Perhaps the folks at Fortune should call us because their research skills are soft. The other day Fortune reported on Quantum Partners' purchase of Violin Memory out of bankruptcy. Of note, QP is a fund tied to billionaire George Soros. The article - not particularly informative in any way whatsoever - doubled-down on its uselessness by noting that "terms of the deal were not disclosed," which, for those of us who know better, reeks of journalistic laziness. Why? Well, of course the terms needed approval by the bankruptcy court and so they were 100% publicly available. $25.6mm (including the DIP/exit facility rollup). Just saying.

Puerto Rico. Apparently it has been a distressed investing quagmire.

Owl Creek Asset Management is shutting down its Asia fund, voluntarily (cough cough) chopping 10% of AUM off. An interesting move considering a general view that there'll be a lot of opportunity there...

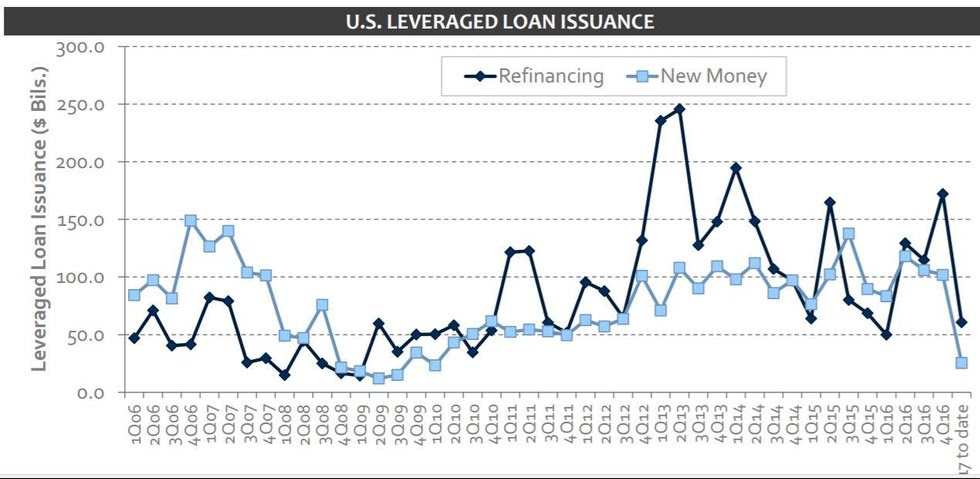

Coal. Prices have risen and Trump is promising assistance. Is this enough to offset sagging demand? China's new measures aren't helping. But the capital markets are, as Peabody Energy, Arch Coal, and Contura Energy are all taking advantage of cheap financing/refinancing options. Peabody shopped an upsized term loan (by $450mm) with revised company-favorable pricing; it also issued new notes and bonds. Amazing how quickly things changed with coal.

Electric Vehicles. Something tells us that oil and gas management teams and their wildly astute restructuring bankers and advisors neglected to bake this element into their business plans.

European Debt. Increasing concerns about Italy and Greece. Meanwhile, in France, CVC Capital Partners' owned vehicle leasing firm Fraikin has hired Rothschild to restructure its 1.4 billion Euro debt. Lazard will represent the mezz debt.

Moelis & Co. & Aramco. "Ken of Arabia"? C'mon, that's just dumb.

Retail. And people wonder why private equity is vilified...case and point: Rackspace. Speaking of private equity, Canada Goose's proposed IPO reeks of a dump-and-run on greater fools. Millennials don't spend money, but Bain Capital will have us believe that $900 fur-lined jackets are the exception to the rule. Riiiight.

Retail Part IV. Amazon announced that the number of third-party sellers on its B2B site has reached 45k, up about 50% from the approx 30k sellers it had at the end of Q2...IN JUNE.

Return of the Maturity Wall. Nothing gets restructuring professionals' juices flowing like sexy maturity stats. So, here it is: $2 trillion of corporate debt comes due in five years. And this is, in part, because the capital markets are definitely wide open right now in the face of soon-to-be rising interest rates. Take THAT wall, President Trump!

Sears. Everyone is looking at this oncoming trainwreck and wondering "when?", not "if." Nice recent CDS movements on it but then the company unearthed a remarkable $1b in cost savings. Like, out of nowhere. And, naturally, the stock soared 25+%.

Spotify. Typically there are tremors before the earthquake. Perhaps Filip Technologies, Violin Memory, and Nasty Gal are the tremors foreshadowing a venture debt-backed reckoning on the horizon. It's unclear. But, in Spotify's case, the interest ratchets attached to $1b of debt get more and more expensive with each consecutive quarter sans IPO. A big "unicorn" is going to fail and fail big. Spotify may not be the one, but it ain't looking great. But that one IS coming (Zenefits anyone?). Along these lines, how the eff is Theranos not bankrupt yet?

Fast Forward: Most retail-focused restructuring pros emphasize "omni-channel," the latest retail buzzword that, practically speaking, means basically nothing in today's climate. Case and point: Neiman Marcus, which was downgraded this week with projected 10x leverage on $4.77b of debt. Most of the cap stack traded at new lows this week. Omni-channel ain't a panacea, it appears.

Rewind I: This result for Relativity Media sure sounds positive.

Rewind II: The grocery space is getting hammered so badly that now even Whole Foods is retrenching, shutting more stores than it's opening go-forward.