Coal. Post-reorg players like Arch Coal are now trying to take advantage ofgovernment subsidy (which reeks of buyside "value-realization"): query what this means for alternative energy players who already receive such subsidies and are rumored to be under siege by the Trump administration...?

Environment. We wrote a few months ago about Oklahoma and the apparent correlation between wastewater disposal and an uptick in seismic activity. The seismic-hazard warning for Oklahoma in 2017 is "still significantly elevated."

Golf & Sexy Time. There's zero correlation: we just thought it was a funny combination. That said, tough times for TaylorMade (owned by Adidas and apparently being shopped by Guggenheim Securities). Meanwhile, Agent Provocateursold while in UK "administration" to an affiliate of Sports Direct (which also recently surfaced as the stalking horse bidder in Eastern Outfitters). AlixPartners was the administrator.

Retail. We're getting a little sick of sounding like a broken record but Best Buyand Targetreported numbers this past week and then saw massive stock drops due to weak guidance. And Barnes & Noblegot DECIMATED after reporting numbers. The good news is that the coloring fad appears to be over. Meanwhile, the tech barrage shows no signs of abating: GameStop came under pressure this week after Microsoftannounced its subscription gaming service. Is GameStop an immediate near term restructuring candidate? No, but part of the value we provide is highlighting for you where future pain points are hiding and without sounding TOO dramatic, this could be the beginning of the end.

Retail II. We're nerds and so we found this analysis of when to close retail stores interesting. And we're curious to know if any of our advisory readers agree with this...LET US KNOW. Speaking of closing retail stores, Abercrombiewill close 60 stores, Crocswill close 160 stores, and looming bankruptcy candidate hhgregg is closing 88 stores (which briefly sent Best Buy's stock north back up, despite earnings). Meanwhile, Neiman Marcus hired Lazard for balance sheet help and Radio Shack2.0 (aka General Wireless Operations) is rumored to be Radio Shack chapter 22.0.

Tech. Rough week for Uber. Choice quote: "Before too long, Uber's cash will run out. And if Uber hasn't built a viable self-driving car by then, the results won't be pretty."

Fast Forward: Seadrill Ltd. noted the possibility of a bankruptcy filing, sending the stock into a tizzy. Still, John Fredriksen quickly highlighted his history of no default. Related, Pacific Drillingalso noted in its earnings call that Chapter 11 is possible.

Rewind I: A lot of folks have been sleeping on tech bankruptcies, but NJOY was a hardware bankruptcy from last year that now has a resolution: Mudrick Capitalseeks to turn the company around, operating it like a PE-owned company rather than a VC-funded company. Speaking of which, Cirque du Soleil got a workover by TPG Capital (and AlixPartners) and now there's this YouTube promotional video to show for it. Speaking of purchases out of bankruptcy, it seems a Canadian retail player made the first move on Wet Seal only to be outflanked by Gordon Brothers.

Rewind II: Soundcloudlooks increasingly like it will be in the busted tech bankruptcy bucket. IP sale?

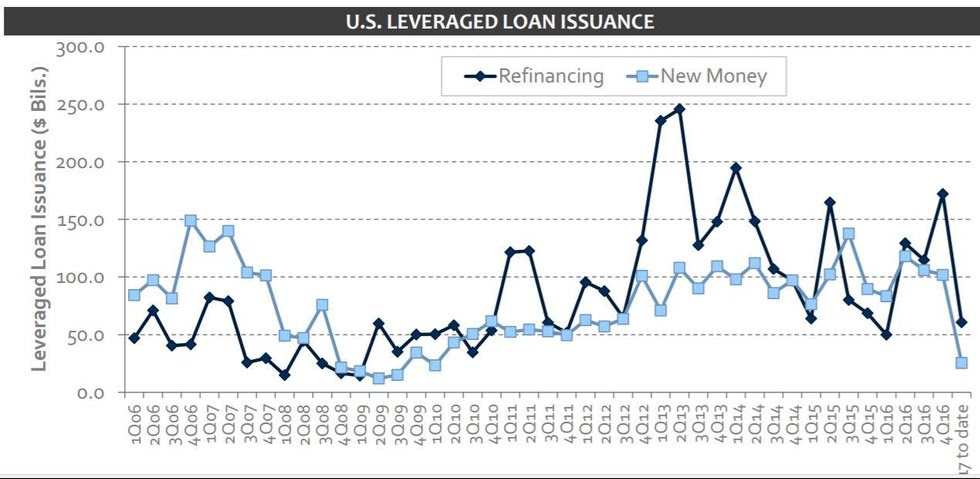

Chart of the Week:

Tweet of the Week: This is great because it doubles as a second chart of the week: we're so creative. Anyway, we hate to say we told you so but, effectively,we told you so: we'd love to know why nearly 200 companies felt the need to reference AI in their earnings reports...

Coal. Prices have risen and Trump is promising assistance. Is this enough to offset sagging demand? China's new measures aren't helping. But the capital markets are, as Peabody Energy, Arch Coal, and Contura Energy are all taking advantage of cheap financing/refinancing options. Peabody shopped an upsized term loan (by $450mm) with revised company-favorable pricing; it also issued new notes and bonds. Amazing how quickly things changed with coal.

Electric Vehicles. Something tells us that oil and gas management teams and their wildly astute restructuring bankers and advisors neglected to bake this element into their business plans.

European Debt. Increasing concerns about Italy and Greece. Meanwhile, in France, CVC Capital Partners' owned vehicle leasing firm Fraikin has hired Rothschild to restructure its 1.4 billion Euro debt. Lazard will represent the mezz debt.

Moelis & Co. & Aramco. "Ken of Arabia"? C'mon, that's just dumb.

Retail. And people wonder why private equity is vilified...case and point: Rackspace. Speaking of private equity, Canada Goose's proposed IPO reeks of a dump-and-run on greater fools. Millennials don't spend money, but Bain Capital will have us believe that $900 fur-lined jackets are the exception to the rule. Riiiight.

Retail Part IV. Amazon announced that the number of third-party sellers on its B2B site has reached 45k, up about 50% from the approx 30k sellers it had at the end of Q2...IN JUNE.

Return of the Maturity Wall. Nothing gets restructuring professionals' juices flowing like sexy maturity stats. So, here it is: $2 trillion of corporate debt comes due in five years. And this is, in part, because the capital markets are definitely wide open right now in the face of soon-to-be rising interest rates. Take THAT wall, President Trump!

Sears. Everyone is looking at this oncoming trainwreck and wondering "when?", not "if." Nice recent CDS movements on it but then the company unearthed a remarkable $1b in cost savings. Like, out of nowhere. And, naturally, the stock soared 25+%.

Spotify. Typically there are tremors before the earthquake. Perhaps Filip Technologies, Violin Memory, and Nasty Gal are the tremors foreshadowing a venture debt-backed reckoning on the horizon. It's unclear. But, in Spotify's case, the interest ratchets attached to $1b of debt get more and more expensive with each consecutive quarter sans IPO. A big "unicorn" is going to fail and fail big. Spotify may not be the one, but it ain't looking great. But that one IS coming (Zenefits anyone?). Along these lines, how the eff is Theranos not bankrupt yet?

Fast Forward: Most retail-focused restructuring pros emphasize "omni-channel," the latest retail buzzword that, practically speaking, means basically nothing in today's climate. Case and point: Neiman Marcus, which was downgraded this week with projected 10x leverage on $4.77b of debt. Most of the cap stack traded at new lows this week. Omni-channel ain't a panacea, it appears.

Rewind I: This result for Relativity Media sure sounds positive.

Rewind II: The grocery space is getting hammered so badly that now even Whole Foods is retrenching, shutting more stores than it's opening go-forward.