July 7, 2019

Back in October 2016, in the context of Sun Capital Partners’-owned Garden Fresh Restaurant Intermediate Holdings bankruptcy filing, we asked, “Are Progressives Bankrupting Restaurants?” We wrote:

Morberg's explanation for the bankruptcy went a step farther. He noted that cash flow pressures also came from increased workers' compensation costs, annual rent increases, minimum wage increases in the markets they serve, and higher health benefit costs -- a damning assessment of popular progressive initiatives making the rounds this campaign season. And certainly not a minor statement to make in a sworn declaration.

It's unlikely that this is the last restaurant bankruptcy in the near term. Will the next one also delineate progressive policies as a root cause? It seems likely.

There have been a plethora of restaurant-related bankruptcy filings between then and now and many of them have raised rising costs as an issue. Perhaps none as blatantly, however, than Sun Capital Partners’ portfolio companies: enter RUI Holding Corp and its affiliated debtors, Restaurants Unlimited Inc. and Restaurants Unlimited Texas Inc. (the “Debtors”).

On July 7, 2019, the Sun Capital-owned Debtors filed for bankruptcy in the District of Delaware. The Debtors opened their first restaurant in 1969 and now own and operate 35 restaurants in 6 states under, among 14 others, the trade names “Clinkerdagger,” “Cutters Crabhouse,” “Maggie Bluffs,” and ”Horatio’s.” The Debtors note that each of their restaurants offer “fine dining” and “polished casual dining” “situated in iconic, scenic, high-traffic locations.” Who knew that if you want something to scream “iconic” you ought to name it Clinkerdagger?

As we’ve said time and time again, casual dining is a hot mess. Per the Debtors:

…the Company's revenue for the twelve months ended May 31, 2019, was $176 million, down 1% from the prior year. As of the Petition Date, the Company has approximately $150,000 of cash on hand and lacks access to needed liquidity other than cash flow from operations.

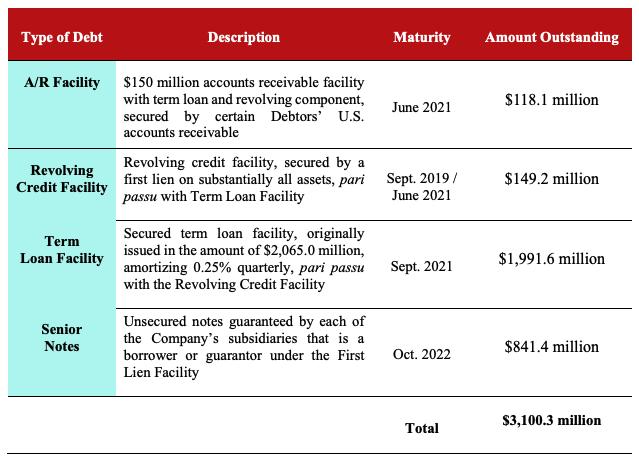

The Debtors have over $37.7mm of secured debt; they also owe trade $7.6mm. There are over 2000 employees, of which 168 are full-time and 50 are salaried at corporate HQ in Seattle Washington.

But enough about that stuff. Back to those damn progressives. Per the Debtors:

Over the past several years, certain changes to wage laws in the Debtors’ primary geographic locations coupled with two expansion decisions that utilized cash flow from operations resulted in increased use of cash flow from operations and borrowings and restricted liquidity. These challenges coupled with additional state-mandates that will result in an additional extraordinary wage hike in FYE 2020 in certain locations before all further wage increases are subject to increases in the CPI and the general national trend away from casual dining, led to the need to commence these chapter 11 cases.

They continue:

Over the past three years, the Company’s profitability has been significantly impacted by progressive wage laws along the Pacific coast that have increased the minimum wage as follows: Seattle $9.47 to $16.00 (69%), San Francisco $11.05 to $15.59 (41%), Portland $9.25 to $12.50 (35%). As a large employer in the Seattle metro market, for instance, the Company was one of the first in the market to be forced to institute wage hikes. Currently in Seattle, smaller employers enjoy a statutory advantage of a lesser minimum wage of $1 or more through 2021, which is not available to the Company. The result of these cumulative increases was to increase the Company’s annual wage expenses by an aggregate of $10.6 million through fiscal year end 2019.

For a second we had to do a double-take just to make sure Andy Puzder wasn’t the first day declarant!

Interestingly, despite these seemingly OBVIOUS wage headwinds and the EVEN-MORE-OBVIOUS-CASUAL-DINING-CHALLENGES, these genius operators nevertheless concluded that it was prudent to open two new restaurants in Washington state “in the second half of 2017” — at a cost of $10mm. Sadly, “[s]ince opening, the anticipated foot traffic and projected sales at these locations did not materialize….” Well, hot damn! Who could’ve seen that coming?? Coupled with the wage increases, this was the death knell. PETITION Note: this really sounds like two parents on the verge of divorce deciding a baby would make everything better. Sure, macro headwinds abound but let’s siphon off cash and open up two new restaurants!! GREAT IDEA HEFE!!

The Debtors have therefore been in a perpetual state of marketing since 2016. The Debtors’ investment banker contacted 170 parties but not one entity expressed interested past basic due diligence. Clearly, they didn’t quite like what they saw. PETITION Note: we wonder whether they saw that Sun Capital extracted millions of dollars by way of dividends, leaving a carcass behind?? There’s no mention of this in the bankruptcy papers but….well…inquiring minds want to know.

The purpose of the filing is to provide a breathing spell, gain the Debtors access to liquidity (by way of a $10mm new money DIP financing commitment from their prepetition lender), and pursue a sale of the business. To prevent additional unnecessary cash burn in the meantime, the Debtors closed six unprofitable restaurants: Palomino in Indianapolis, Indiana, and Bellevue, Washington; Prime Rib & Chocolate Cake in Portland, OR; Henry’s Tavern in Plano, Texas; Stanford’s in Walnut Creek, California; and Portland Seafood Co. in Tigard, Oregon. PETITION Note: curiously, only one of these closures was in an “iconic” location that also has the progressive rate increases the Debtors took pains to highlight.

It’s worth revisiting the press release at the time of the 2007 acquisition:

Steve Stoddard, President and CEO, Restaurants Unlimited, Inc., said, “This transaction represents an exciting partnership with a skilled and experienced restauranteur that has the requisite financial resources and deep operating experience to be instrumental in strengthening our brands and building out our footprint in suitable locations.”

Riiiiight. Stoddard’s tenure with Sun Capital lasted all of two years. His successor, Norman Abdallah, lasted a year before being replaced by Scott Smith. Smith lasted a year before being replaced by Chris Harter. Harter lasted four years and was replaced by now-CEO, Jim Eschweiler.

A growing track record of bankruptcy and a revolving door in the C-suite. One might think this may be a cautionary tale to those operators in the market for PE partners.*

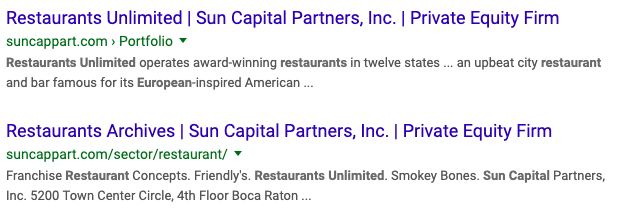

*Speaking of geniuses, it’s almost as if Sun Capital Partners thinks that things disappear on the internets. Google “sun capital restaurant unlimited” and you’ll see this: