🌑New Chapter 11 Bankruptcy Filing - Blackhawk Mining LLC🌑

Blackhawk Mining LLC

July 19, 2019

What are we averaging? Like, one coal bankruptcy a month at this point? MAGA!!

This week Blackhawk Mining LLC filed prepackaged Chapter 11 cases in the District of Delaware, the effect of which will be the elimination of approximately $650mm of debt from the company’s balance sheet. Unlike other recent bankruptcies, i.e., the absolute and utter train wreck that is the Blackjewel LLC bankruptcy, this case actually has financing and employees aren’t getting left out in the lurch. So, coal country can at least take a deep breath. Small victories!

Before we get into the mechanics of how this deleveraging will work, it’s important to note some of the company’s history. Blackhawk represents opportunism at its best. Founded in 2010 as a strategic vehicle to acquire coal reserves, active mining operations and logistical infrastructure located primarily in the Appalachian Basin, the privately-owned coal producer hit the ground running. Initially the company started with Kentucky thermal coal assets (PETITION Note: thermal coal’s end use is the production of electricity; in contrast, metallurgical coal’s prime use is for the production of steel). It then quickly moved to diversify its product offering with a variety of acquisitions. In 2014, it acquired three mining complexes in the bankruptcy of James River Coal Company (which served as the company’s entry into the production of met coal). Thereafter, in 2015, the company purchased six mining complexes in the bankruptcy of Patriot Coal Company (which has since filed for bankruptcy a second time). This acquisition lofted the company into the highest echelon of US-based met coal production (PETITION Note: met coal drives 76% of the company’s $1.09b in revenue today). The company now operates 19 active underground and 6 active surface mines at 10 active mining complexes in West Virginia and Kentucky. The company has 2,800 employees.

Naturally, this rapid growth begs some obvious questions: what was the thesis behind all of these acquisitions and how the hell were they financed?

The investments were a play on an improved met coal market. And, to some degree, this play has proven to be right. Per the company:

“The Company’s strategic growth proved to be a double-edged sword. On one hand, it significantly increased the Company’s position in the metallurgical coal market at a time when asset prices were depressed relative to today’s prices. The Company continues to benefit from this position in the current market. The price of high volatile A metallurgical coal has risen from $75 per ton to an average of $188 per ton over the last two years, providing a significant tailwind for the Company. On the other hand, the pricing environment for metallurgical coal did not improve until late 2016, and the debt attendant to the Company’s acquisition strategy in 2015 placed a strain on the Company’s ability to maintain its then-existing production profile while continuing to reinvest in the business. During this time, to defer expenses, the Company permanently closed over 10 coal mines (with over 5 million tons of productive capacity), idled the Triad complex, and depleted inventories of spare equipment, parts, and components. Furthermore, once the coal markets began to improve, the Company was forced to make elevated capital expenditures and bear unanticipated increases in costs—for example, employment costs rose approximately 25% between 2016 and 2018—to remain competitive. The confluence of these factors eventually made the Company’s financial position untenable.”

Longs and shorts require the same thing: good timing.

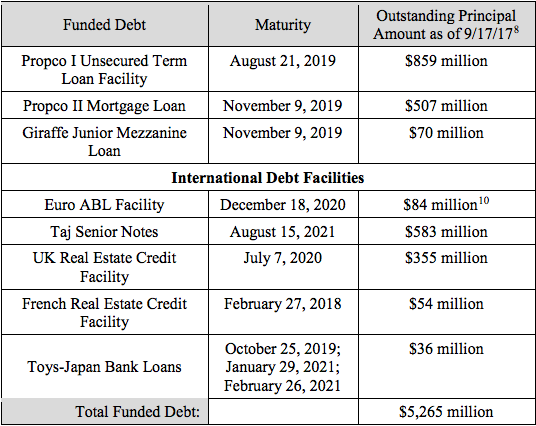

Alas, the answer to the second question also leads us to the very predicament the company finds itself in today. The company has $1.09b in debt split across, among other things, an ABL facility (’22 $85mm, MidCap Financial LLC), a first lien term loan facility (’22 $639mm, Cantor Fitzgerald Securities), a second lien term loan facility (’21 $318mm, Cortland Capital Markets Services LLC), and $16mm legacy unsecured note issued to a “Patriot Trust” as part of the Patriot Coal asset acquisition. More on this Trust below.

But this is not the first time the company moved to address its capital structure. In a bankruptcy-avoiding move in 2017, the company — on the heals of looming amortization and interest payments on its first and second lien debt — negotiated an out-of-court consensual restructuring with its lenders pursuant to which it kicked the can down the road on the amortization payments to its first lien lenders and deferred cash interest payments to its second lien lenders. If you’re asking yourself, why would the lenders agree to these terms, the answer is, as always, driven by money (and some hopes and prayers). For their part, the first lien lenders obtained covenant amendments, juiced interest rates and an increased principal balance owed while the second lien lenders obtained an interest rate increase. Certain first and second lien lenders also got equity units, board seats and additional voting rights. These terms — onerous in their own way — were a roll of the dice that the environment for met coal would continue to improve and the company could grow into its capital structure. Clearly, that hope proved to be misplaced.

Indeed, this is the quintessential kick-the-can-down-the-road situation. By spring 2019, Blackhawk again faced a $16mm mandatory amortization payment and $20mm in interest payments due under the first lien term loan.

Now the first lien lenders will swap their debt for 71% of the reorganized equity and a $225mm new term loan and the second lien lenders will get 29% of the new equity. The “will-met-coal-recover-to-such-a-point-where-the-value-of-the-company-extends-beyond-the-debt?” option play for those second lien lenders has expired. The company seeks to have its plan confirmed by the end of August. The cases will be financed by a $235mm DIP of which $50mm is new money and the remainder will rollup $100mm in first lien term loan claims and $85mm in ABL claims (and ultimately convert to a $90mm exit facility).

Some other quick notes:

Kirkland & Ellis LLP represents the company after pushing Latham & Watkins LLP out in a move that would make Littlefinger proud. This is becoming an ongoing trend: as previously reported, K&E also gave das boot to Latham in Forever21. A war is brewing folks.

The Patriot Trust will get $500k per a settlement baked into the plan. On a $16mm claim. The “Patriot Trust” refers to the liquidating trust that was established in connection with the Patriot Coal Corporation chapter 11 cases, previously filed in the Eastern District of Virginia. Marinate on that for a second: the creditors in that case fought long and hard to have some sort of recovery, won a $16mm claim and now have to settle for $500k. There’s nothing like getting screwed over multiple times in bankruptcy.

But then there’s management: the CEO gets a nice cushy settlement that includes a $500k payment, a seat on the reorganized board of managers (and, presumably, whatever fee comes with that), and a one-year consulting contract. He waives his right to severance. If we had to venture a guess, Mr. Potter will soon find his way onto K&E’s list of “independent” directors for service in other distressed situations too. That list seems to be growing like a weed.

Knighthead Capital Management LLC and Solus Alternative Asset Management LP are the primary holders of first lien paper and now, therefore, own the company. Your country’s steel production, powered by hedge funds! They will each have representation on the board of managers and the ability to jointly appoint an “independent” director.

Jurisdiction: D. of Delaware (Judge Silverstein)

Capital Structure: See above.

Professionals:

Legal: Kirkland & Ellis LLP (James Sprayragen, Ross Kwasteniet, Joseph Graham, Stephen Hessler, Christopher Hayes, Derek Hunter, Barack Echols) & (local) Potter Anderson Corroon LLP (Christopher Swamis, L. Katherine Good)

Financial Advisor: AlixPartners LLP

Investment Banker: Centerview Partners (Marc Puntus)

Claims Agent: Prime Clerk LLC (*click on the link above for free docket access)

Other Parties in Interest:

Prepetition ABL & DIP ABL Agent: Midcap Funding IV Trust

Legal: Hogan Lovells US LLP (Deborah Staudinger)

Prepetition & DIP Term Agent: Cantor Fitzgerald Securities

Legal: Herrick Feinstein LLP (Eric Stabler, Steven Smith)

Second Lien Term Loan Agent: Cortland Capital Market Services LLC

Legal: Stroock & Stroock & Lavan LLP (Alex Cota, Gabriel Sasson)

Consenting Term Lenders: Knighthead Capital Management LLC, Solus Alternative Asset Management LP, Redwood Capital Management LLC

Davis Polk & Wardwell LLP (Brian Resnick, Dylan Consla, Daniel Meyer)

Ad Hoc Group of First Lien Lenders

Legal: Shearman & Sterling LLP (Fredric Sosnick, Ned Schodek)