Other reports substantiate these trends. Per RetailDive:

It's still not a pretty picture on the ground, however. Second quarter mall rents fell 4.6% from the first quarter and 7.1% year over year, hit by major store closures from Toys R Us, Sears and J.C. Penney, according to a trend report from commercial real estate firm JLL. Mall vacancy rates hit 4% during the period, JLL said. The retail sector suffered its worst quarter in nine years with net absorption of negative 3.8 million square feet, which pushed the regional mall vacancy rate up by 0.2% to 8.6% as the average mall rent increased 0.3%, according to another report from commercial real estate firm Reis emailed to Retail Dive.

And things have gotten worse since then. On October 3, four days before the Axios piece, The Wall Street Journal reported on Q3 numbers:

Mall vacancy rates rose to 9.1% in the third quarter, their highest level in seven years. Many of the older shopping centers that lack trendy retailers, lively restaurants, or other forms of popular entertainment continue to lose tenants, or even close down.

But many lower-end malls are still struggling to benefit from the economic revival, especially in some of the more economically depressed areas in Pennsylvania, Ohio and Michigan. They suffer from a glut of shopping centers but not enough consumers.

The average rent for malls fell 0.3% to $43.25 a square foot in the third quarter, down from $43.36 in the second quarter, according to data from real-estate research firm Reis Inc. The last time rents slid on a quarter-over-quarter basis was in 2011.

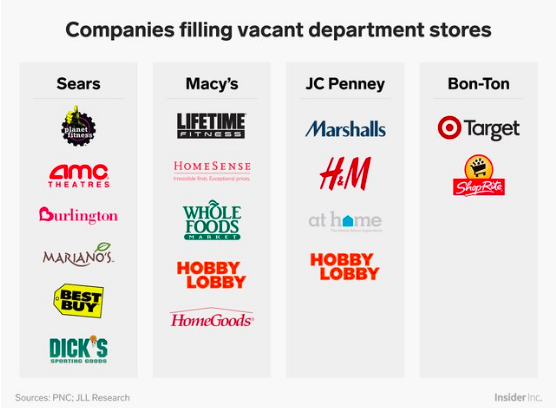

What sparked the vacancy jump? Bankrupted Bon-Ton Stores closing and, gulp, Sears closures too. Which, obviously, could get a hell of a lot worse. Indeed, Cowen and Company recently concluded that “we are only in the ‘early innings’ of mass store closures.” As noted in Business Insider:

"Retail square footage per capita in the United States has been widely sourced and cited as being far above most developed countries — more than double Australia and over four times that of the United Kingdom," Cowen analysts wrote in a 50-page report on the state of the retail industry. The data "suggests that the sector remains in the early innings of reduction in unproductive physical retail."

On point, one category that had largely remained (relatively) unscathed in the last 2 years of retail carnage is the home goods space. But, now, companies like Pier 1 Imports Inc. ($PIR) and Bed Bath & Beyond Inc. ($BBBY) appear to be in horrific shape. Bloomberg’s Sarah Halzack writes:

Two major companies in this category, Bed Bath & Beyond Inc. and Pier 1 Imports Inc., are mired in problems that look increasingly unsolvable. Bed Bath & Beyond saw its shares tumble 21 percent on Thursday after it reported declining comparable sales for the ninth time in 10 quarters. And Pier 1’s stock fell nearly 20 percent in a single day last week after it saw an even ghastlier plunge in same-store sales and discontinued its full-year guidance.