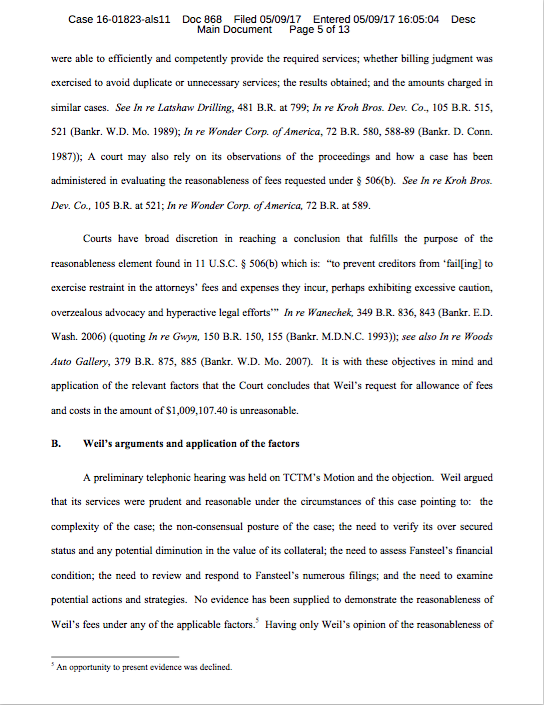

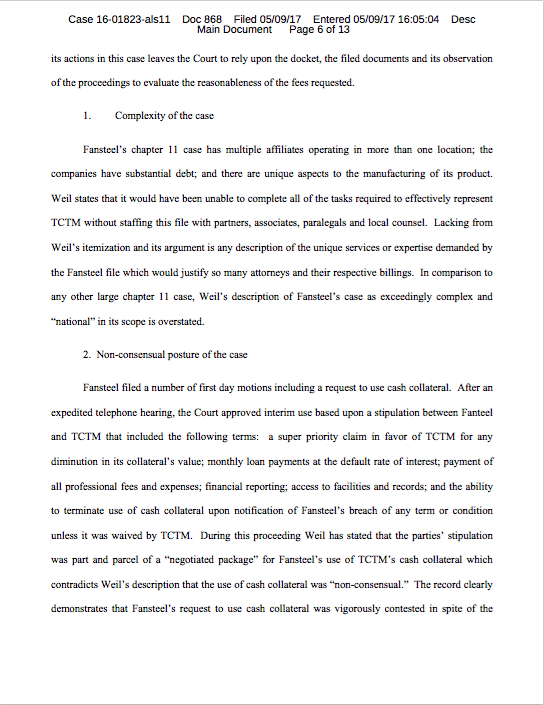

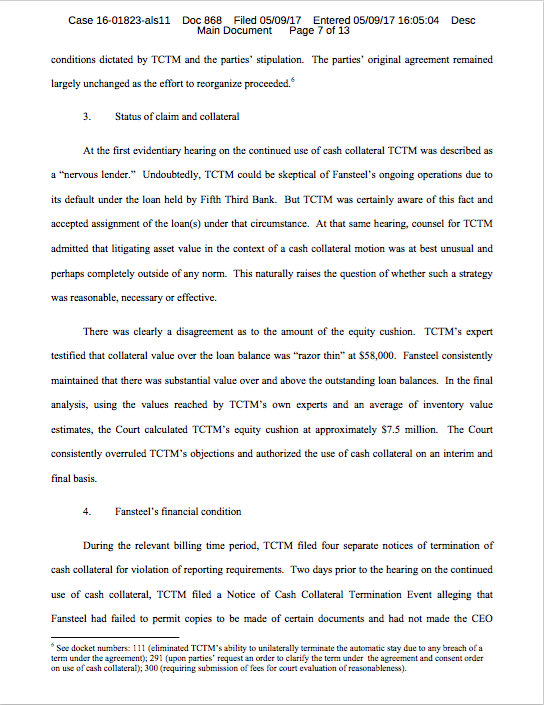

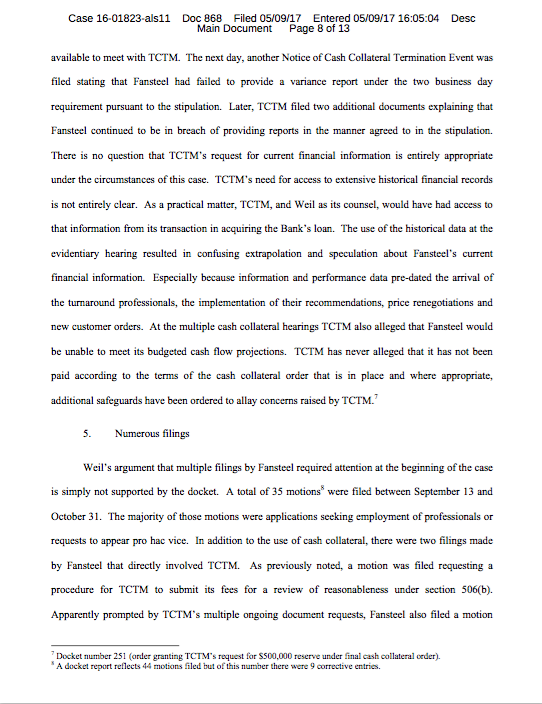

Like #Tech, Corporate Restructuring Has a Gender Imbalance

Unless you've been hiding under a rock, you've probably noticed the controversy that embroiled Silicon Valley over the July 4th weekend. In a nutshell, some super brave and bada$$ women came forward and accused a variety of high-powered men of sexual harassment and improper behavior. First, The Information reported (firewall) a story backed by the accounts of six women recounting the behavior of Justin Caldbeck of Binary Capital. He soon stepped down (as did his two partners, thus thwarting the close of BC's second fund). Then The New York Times published a piece implicating Chris Sacca (of Shark Tank fame) and Dave McClure of the venture capital firm, 500 Startups. The former had already given up on investing (and Shark Tank); the latter first stepped down as CEO of the firm, then, in a matter of days, stepped down as General Partner as well. Silicon Valley's gender imbalance has been in the spotlight for some time now. Now we're learning more and more why that imbalance exists in the first place.

Before we get ahead of ourselves, we'll be upfront here: what we're about to say is in no way meant to imply that sexual harassment and inappropriate behavior runs rampant in the restructuring community. But, let's be honest: there is a wild gender imbalance in firm partnership ranks, conference room negotiations, and bankruptcy courts. The industry's most lucrative and prolific restructuring law firm has exactly one woman partner. One of the industry's top restructuring advisory IBs has exactly zero women partners and, yet, that didn't stop the leader of that group from being honored by Her Justice, an organization that provides legal services to NYC women in need. And those are just two examples. Suffice it to say, there are many.

Now there are exceptions to the general rule: AlixPartners LLC, for one, and Greenberg Traurig LLP, for another (see below), in that they are led (or co-led as the case may be) by women. Weil Gotshal & Manges LLP, as another example, includes a number of women partners on its roster. But there should be more. Industry-wide. And charity honorees should be the women who have risen through the ranks - despite the odds - AND cultivated other women to follow in their footsteps. Overall, the industry can do much much better.

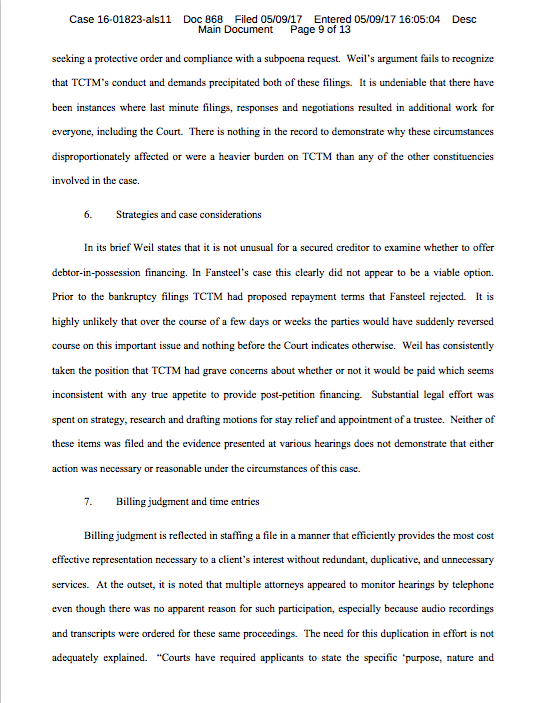

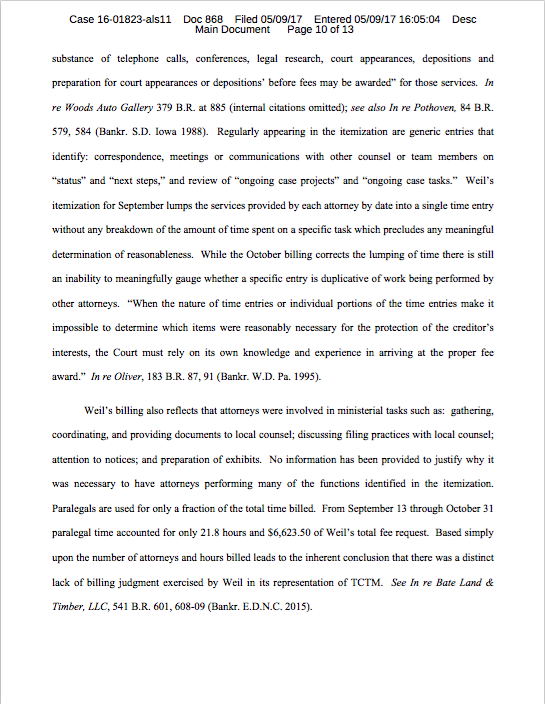

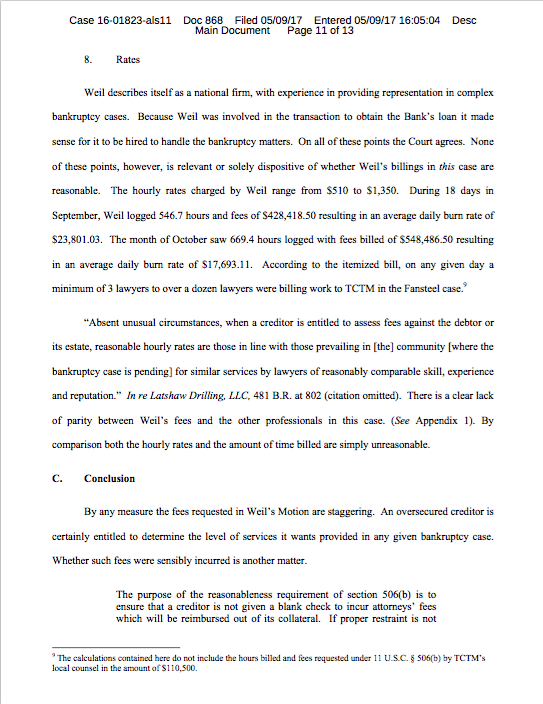

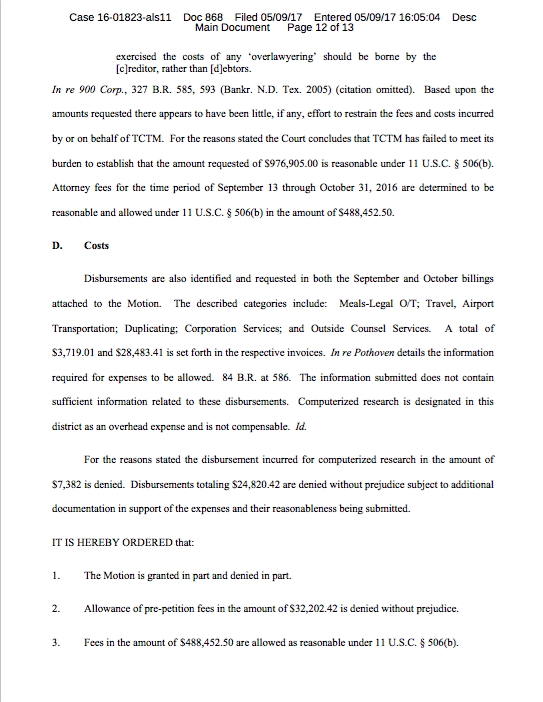

Want to tell us we're morons? Or praise us? Cool, either way: email us.